Whilst many people may be struggling to keep up payments on their mortgages in the wake of steep interest rate rises, there are a significant number of homeowners who may be wondering whether it is worthwhile paying more than the minimum statutory repayments each month, with the aim of helping to save money in the long run.

We look at some of the pros and cons of making a mortgage overpayment each month to see whether the average homeowner could be better or worse off by making an additional payment each month, along with comparing overpayments to saving/investing your money instead.

How to Make a Mortgage Overpayment

We’re all different, with different circumstances, so it’s wise to seek professional advice and guidance before deciding to arrange a mortgage overpayment. Your existing mortgage lender is likely to have some advice on their website, but we’d also advise that you talk to us too. We’ll be able to look at your precise circumstances and help give an illustration of what you can achieve by making an overpayment that suits your own lifestyle needs.

How Much Can You Overpay?

The amount can be whatever you can manage, whether a small amount, right up to a general maximum of around 10% of the remaining balance each year1. Overpayments above this maximum amount can be liable for early repayment charges from your lender, so it’s wise to consider this before setting a precise amount. We can help you find the optimum amount that you’d like to repay each month by working with you – simply contact us to arrange an appointment accordingly.

When deciding how much to overpay, it’s important to consider the level of disposable income that you need to enjoy your current lifestyle, and especially any forthcoming expenditures – for example, having money set aside for any family holidays, activities, vehicle maintenance bills or household issues, for example.

What Are the Benefits of Overpaying?

Aside from reducing your mortgage debt more quickly, and potentially saving money on the amount of interest owed, there are additional benefits that can be seen from overpaying your mortgage.

- If your mortgage rate is higher than your savings rate, you may find that it is more beneficial to pay back the mortgage and reduce the interest owed, compared to the amount of interest that your money may make while it is sitting in a bank account.

- If you pay more of your mortgage off sooner, this can sometimes put you in a stronger position for a cheaper mortgage deal when your existing one is due for renewal. This is because you will have more equity in your property, and your loan-to-value (LTV) is decreased, which often opens up more choices when it comes to available rates for mortgages.

What Are the Drawbacks of Overpaying?

If you have other debts which have higher interest rates, such as credit cards or additional loans, then it may be more beneficial to pay these off first. It’s worth considering any other costs you are likely to incur, and factoring these into whether you can afford to make a mortgage overpayment each month.

With interest rates rising, it’s also worthwhile doing your homework to see what your money could earn you if it’s saved in a high-interest account – there are chances that in some cases it may be more beneficial to save your money rather than pay additional amounts on your mortgage.

It’s important to think carefully about the amounts of money that you may wish to utilise on either overpaying or saving before going further, before looking at the various options available to you. It could be worth seeking financial advice for this element before making a decision.

As mortgage advisers, we are able to assist you in the area of what your mortgage circumstances may look like if you were to consider an overpayment, the impact that this could make on your mortgage and assistance in how you go about facilitating this.

Your home may be repossessed if you do not keep up repayments on your mortgage.

How Much Will I Save By Overpaying My Mortgage? (Example)

Here’s a few simplified examples to show how it could work –

If someone had a £150,000 mortgage, with a term of 20 years at a rate of 5%, they’d be required to pay back a total of £237,584 in total when making the contracted standard repayment each month.

However, if they made an extra monthly overpayments stated below, here is how much they could save based on the amount they overpay.

This table shows you the true impact it can have over a long period of time:

Quick note: These are approximate figures (rounded), but they give a clear picture of how even small overpayments can save thousands in interest and cut years off your mortgage.

Of course, you have to remember that, naturally, there are more complexities in real life, and there are fluctuating rates each time you remortgage.

Generally, though, it goes to show that in many cases it may be possible to pay off a mortgage faster and reduce the amount of interest paid by making relatively small extra overpayments each month.

Should You Overpay Your Mortgage or Save?

Whether you should overpay your mortgage or put money into a high yield savings account depends on many factors, but more often than not, overpaying your mortgage beats saving.

The bottom line on this is that if your mortgage rate is higher than your savings rate, overpaying almost always wins, because the “return” is guaranteed and tax-free.

Whereas, if your savings rate is higher than your mortgage rate, then you can earn more saving, but there are more potential tax implications on your savings unless you use ISA products.

In our opinion, you should make sure to balance your savings and overpayments, because it’s always useful to have a buffer of savings on hand at any time in case of emergencies such as job loss.

To get personalised advice on your own situation, though, I’d recommend speaking to the team here at Bell Financial Solutions, as this information can often be generalised.

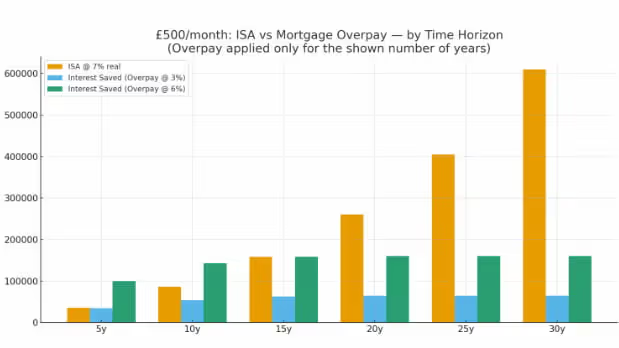

Should You Overpay Your Mortgage or Invest?

Now, this is where it gets interesting. There is a new debate that has arisen over the past decade on whether you should overpay your mortgage or invest your money…

Overpaying vs Investing: A Closer Look

Before we get into this, this is only going to be based on past performance, which does not guarantee future results. Furthermore, money isn’t just about numbers on a spreadsheet, it’s about your risk tolerance and what you want in your own life.

If paying off your mortgage is important to you so you have less of a burden every month, then this may be the way forward for you. However, with investing, could you have compounded your money over that time and made more overall capital?

That’s what we’ll look at here - we’ll be comparing overpaying your mortgage with investing in an S&P 500 ETF (exchange traded fund), which has been the benchmark of investing for the last 100+ years:

Disclaimer: It shows the differences between how the case for investing becomes a stronger case with a lower mortgage rate and staying invested over a long period of time. Remember though, when investing, your capital is at risk. Past performance is not a guarantee of future results, and you should always do your own research.

Our Prevailing Thoughts

Overall, it is ultimately your decision whether you overpay your mortgage or not. Personal finances are personal for a reason and even if the numbers don’t sometimes make sense, if it’s what makes you feel better and more stable, then do what works for you.

Overpaying your mortgage is definitely a great way to save some cash, reduce your mortgage term, will help the remortgage process, and many more. Over a long period of time, overpaying typically beats saving… but not investing on the spreadsheet.

As we said previously though, it’s your decision and if you want help making that decision, the team here at Bell Financial Solutions are always on hand to help!

Overpaying Mortgage FAQs

.avif)