In the United Kingdom, we have a dual healthcare system: the National Health Service (NHS) provides public healthcare, while private medical insurance offers an alternative for those seeking additional benefits and faster access to medical services.

In this blog, we're going to be looking at what private health insurance is, how the cost is calculated, the actual cost of private medical insurance in the UK (the average by age), and many more factors to keep in mind when choosing your very own plan.

What is Private Health Insurance?

Private health insurance (or you may know as ‘private medical insurance’) is basically a policy in which you pay for to be treated privately. Essentially, it’s just the bill you’ll have to cover if you want to be treated privately and quickly, rather than through the public service.

You have the freedom to choose this rather than the NHS, but it will come at a steeper cost, which we’ll go through later on in this article.

What is Typically Covered in a Private Health Insurance Policy?

For most private insurance policies, here are the most common needs that are covered:

- Treatment in a private hospital/centre rather than a public hospital

- Often, you get access to digital healthcare

- Private 1-on-1 consultations

- Diagnostic tests (MRI scans, CT scans, etc)

- Physiotherapy

- Inpatient and outpatient care

- Mental health cover

- Surgery

This is just some of the cover you can expect to get from the majority of policies you potentially choose to go with.

Why Are People in the UK Turning to Private Health Insurance?

People are now turning to private health insurance more and more due to the long waiting times to get an appointment at the NHS. This has been happening for a while, but the COVID-19 pandemic has definitely been the main contributing factor to the backlog in medical treatment.

As of July 2025, the latest figures we have are that there are 7.36 million patient pathways on the list for consultant-led treatment, with around 6.25 million being individual patients. They seem to be lowering every month, with this being the lowest we’ve seen since March 2023, but, unfortunately, it’s still far too high.

Pros and Cons of Private Medical Insurance

There are pros and cons to paying for the cost of private medical insurance, which we’ll go through more here:

Pros

- One of the primary advantages of private medical insurance is quicker access to medical consultations, tests, and treatments. This can be especially beneficial when facing non-life-threatening conditions that still require prompt attention

- Private insurance can allow you to choose the specialists you want to see and the hospitals you prefer. This level of choice can be valuable if you have specific medical needs or prefer a particular healthcare facility

- Depending on the plan you choose, private medical insurance can cover a wide range of services, including diagnostics, surgeries, therapies, and sometimes even dental and optical care

- Many private insurance plans cover private rooms during hospital stays, offering more comfort and privacy compared to shared NHS wards

- While the NHS provides excellent care, some elective procedures might have longer waiting times. Private insurance can help you skip these waiting lists and receive treatment sooner.

Cons

- Chronic illnesses aren’t typically covered in the policies, so you may find difficulty using private medical insurance in this case

- A pre-existing medical condition you already had prior to private healthcare will most likely not be covered in the new policy (and if so, it’ll be a lot more expensive)

- Depending on your location, there may not be any private healthcare locations really close to you, which may affect time in your day

- Some private health insurance can be really expensive, depending on the factors discussed a bit later, so it’s not an option for everyone in the UK

- If you have a serious illness, sometimes, the NHS can actually provide better healthcare, as you’ll be put on the NHS priority treatment list.

How is the Cost Of Private Health Insurance Calculated?

- Age and health status - Age and health status are huge factors in PMI costs. Younger individuals generally pay lower prices, whereas older individuals may experience higher prices. Additionally, your overall health status, medical history, and any pre-existing conditions can impact the premium you'll be charged

- Who and what you cover - The extent of who and what you cover in your insurance will determine your costs. Similar to mortgage insurance, you may want to add more or additional people

- The excess you choose - Excesses are the amount you need to pay before your coverage kicks in. Plans with higher excess usually have lower premiums, but you'll need to pay more out-of-pocket when you receive care and vice versa

- Location - Healthcare costs can change massively by location, so if you live in an area with higher medical expenses, your PMI premium might reflect these higher costs

- Network of providers - If you plan offers access to a broad network of doctors and hospitals, it typically comes with higher premiums and vice versa

- What add-ons you choose - Additional benefits such as wellness programs, gym memberships, and mental health coverage can influence the cost

- Family cover - If you insure a family member on your policy, it will come with increased costs due to the broader coverage needed

- The provider you pick - Different insurance companies offer different pricing structures for PMI, so it’s worth shopping around.

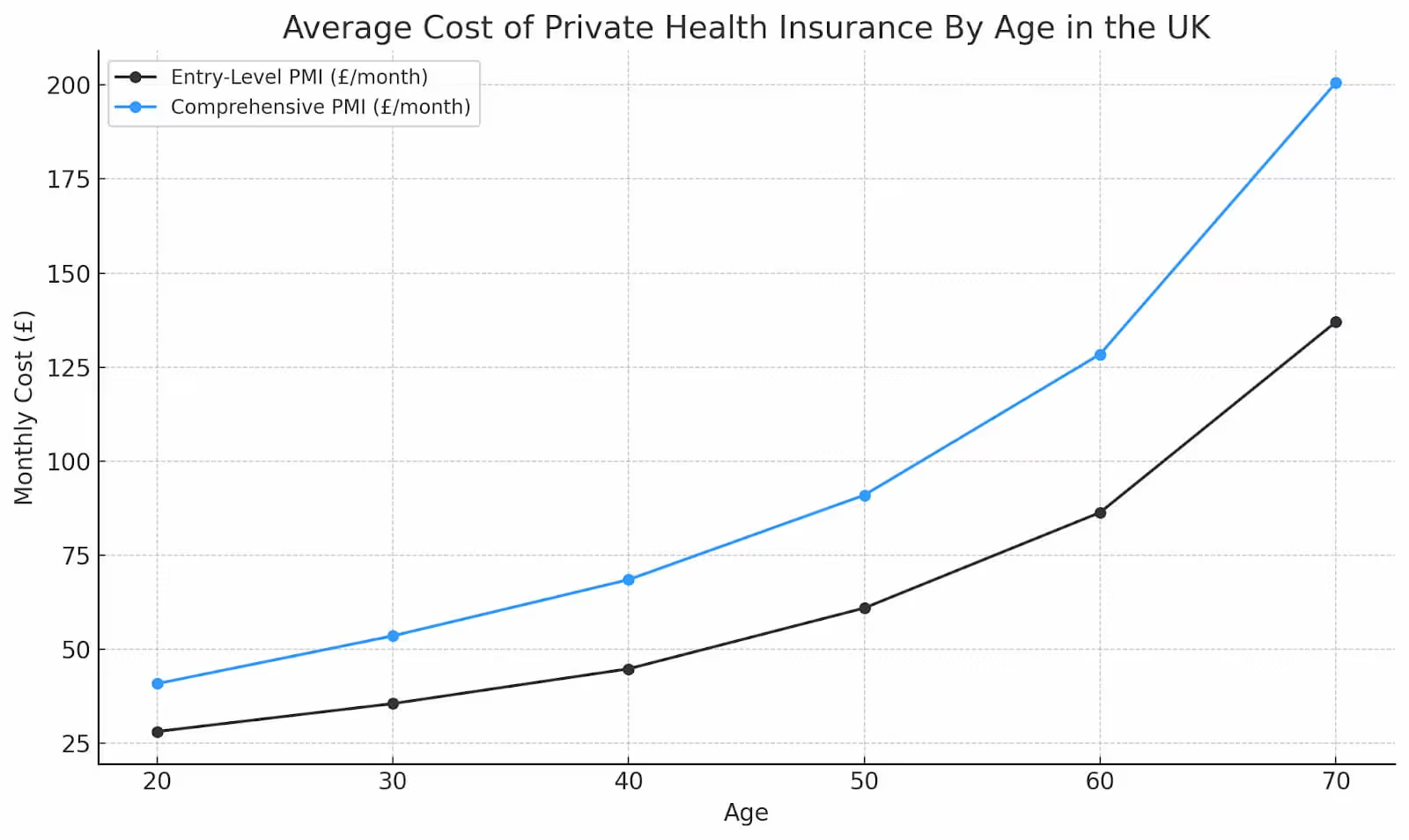

Average Cost of Private Health Insurance By Age in the UK

Below is the average cost of private health insurance by age in the UK:

Comparing the Best Private Health Insurance Providers

Here, we’re going to run through some of the most reputable private health insurance providers in the country and give you unbiased thoughts on them all so you make the best decision for you:

Things You Should Look at Before Going Private

Before you look at going private for you or your loved ones, it’s definitely worth considering all of the below factors first:

#1 The Coverage You Get

Different plans offer varying degrees of coverage, so definitely take a deeper look into your own medical needs and preferences when selecting a plan. Some policies might cover only essential medical services, while others provide much larger-scale coverage.

#2 The Cost

The cost of private insurance can vary based on factors such as your age, health status, and the level of coverage you choose, as we discussed previously, so remember to balance the costs with the potential benefits you’re going to get.

#3 Is Your Health Issue Pre-Existing?

As we looked at previously, some insurers might exclude coverage for pre-existing conditions or charge higher premiums if you have existing health issues. Make sure to understand the policy's stance fully on pre-existing conditions.

#4 Look at the Convenience and Facilities

You should definitely make sure that the facilities are conveniently located for you near your home or home you're moving to, especially if you’re regularly visiting the hospital or treatment centre. Make sure all of it suits your needs and has everything in place for it to be a great experience for you and whoever you add to the policy (if you’ve chosen to).

#5 The Waiting Periods

Some policies have waiting periods for certain treatments or conditions, so you need to make sure you're aware of these waiting periods, as they might affect the immediate availability of coverage for your specific health issue.

#6 Look at What is and Isn’t Included

Oftentimes, people will choose a policy without deeply researching what’s actually included and will be unpleasantly surprised by their health issue not even being covered in the plan. Make sure to do your due diligence and pick a plan that’s right for you, all around.

How Much Does an Individual Private Healthcare Treatment Cost?

According to research done by MyTribe Insurance, here are the average costs of some of the most common private healthcare treatments in the UK:

Our Roundup

Overall, private health insurance in the UK offers individuals an alternative to the NHS, providing faster access to medical services, a choice of specialists, and additional coverage options that you otherwise wouldn’t have.

Your best bet is to research different plans, compare quotes, and consult with insurance providers to find the best fit for your healthcare needs. If you need some help, It’s not just as easy as picking a private health insurance plan and then just choosing the first one you see. There are certainly factors you should look at before going private:

Remember that private medical insurance is an investment in your health and well-being. So, whether you choose to or not to go private, it’s ultimately your decision and doing what’s right for you and the people around you is always the best decision.

.avif)